home

about

our services

our process

our team

our locations

INSIGHTS

client login

Case Studies

careers

get started

"This is a quote from a Coyle Leader. These can appear randomly from a few select quotes."

The year was 1626, and Sweden’s King Gustavus Adolphus was in the middle of a war with Poland to control trade routes and ports on the Baltic Sea. To improve his naval capabilities, the king ordered the construction of a series of large, three-masted warships. One of these was built with two gun decks, the second required to accommodate the king’s order to install seventy-two 24-pound guns. It would be the most powerful warship in the world when completed. Work began that year on the first ship, Vasa, and as her construction dragged on for two years, the king became increasingly impatient to have the warship put to sea.

The King’s new flagship began its maiden voyage on August 10, 1628, and as the ship left the harbor, the deck gun ports were opened to fire off a salute for the onlookers. Once out of the harbor, Vasa’s sails immediately filled with the wind blowing from nearby bluffs. The ship suddenly heeled to port, so much so that the opened lower deck gun ports went underwater, quickly filling the hold of the ship with sea water. 1,400 yards into her maiden voyage, the Vasa sank within minutes to the bottom of Stockholm harbor.

An inquest into the disaster was held later that year. A senior Swedish naval officer gave a succinct explanation for why Vasa sank: the ship did not have enough “belly to carry the upperworks.” In other words, Vasa was severely top-heavy, with the center of gravity too high relative to the center of buoyancy, making it unstable even in moderate waves and winds (1)

333 years later, the wreck of the Vasa was recovered and is now displayed at the Vasa Museum in Stockholm, where it is a testimony to the flawed state of 17th century shipbuilding ideas. A century later, the use of water ballast (pumped into tanks) to manage ship stability became widespread. Adding weight through ballast tanks to manage a ship’s center of gravity is now an accepted shipbuilding principle, helping vessels resist capsizing or excessive rolling in rough seas.

Interesting naval history, perhaps, but what does it have to do with investing? I’m glad you asked. The concept of ballast is akin to the important role that bonds and liquidity reserves (i.e., money market funds or cash) can play in an investment portfolio. Think of the market volatility that naturally comes with stocks in a portfolio (the “ship”), with higher equity allocations resulting in greater “instability.” Adding bonds or cash to the portfolio (the “ballast”) can reduce overall volatility and provide a more stable investment experience over time.

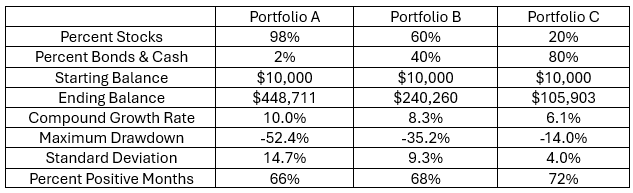

The following table illustrates the idea as we go from a 98% equity portfolio (2% cash) to portfolios containing 40% and 80% bond/cash allocations, respectively. The historical data summarized in this table are for the 40-year period ending 12/31/25 for a diversified portfolio [2]

Two things should be readily apparent as you scan across the three portfolios. First, equities are the engine of wealth creation in a portfolio. The higher the equity allocation, the higher the portfolio’s compounded annual return, from 6.1% to 10.0% per annum. Second, the higher the percentage of bonds and cash, the lower the volatility of the portfolio, as seen in the last three variables: maximum portfolio drawdown (from −52% to −14%), standard deviation (a statistical measure of the dispersion of returns) (from 15% to 4%), and percent of positive return months out of 480 total months (from 66% to 72%). Higher expected returns come with a broader range of potential returns from year to year and larger potential drawdowns.

Helping to explain this pattern is the fact that high-grade, short-to-intermediate maturity bond prices exhibit much lower volatility than equities. Another factor to consider is the inverse movement of bond prices relative to stocks, which can occur when equities sell off. The common rationale for this is that when investors shift to a “risk-off” mentality and fear replaces greed, many investors sell equities and reinvest in the relative safety of high-grade bonds, driving up bond prices. Historically, bonds have been a good diversifier in a portfolio when equities become volatile.

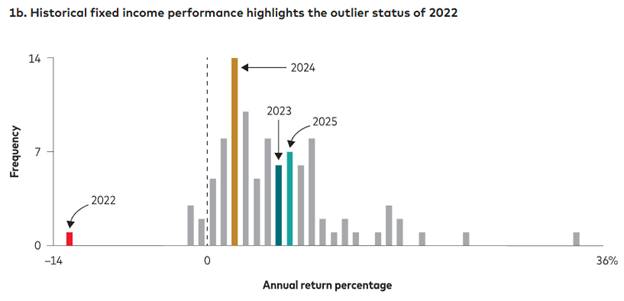

Since 1979, there have been only five years (out of 47 total) in which U.S. bonds had a negative calendar return, the most recent being 2022, when both bonds and stocks ended the year in the red. As you may recall, the Federal Reserve raised overnight interest rates over 5% to combat rampant inflation. To put that year in perspective, here is a chart showing the frequency of calendar-year U.S. bond total returns since 1928. Notice where 2022 appears—a far-left outlier (in red) compared to the much larger cluster of positive-return years:

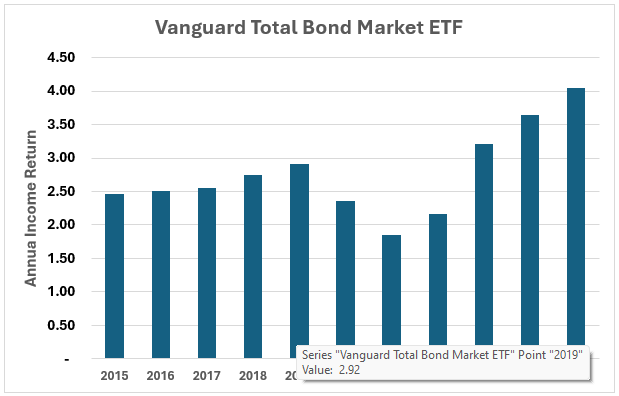

One final consideration for having bonds in a portfolio, besides their ballast and diversification benefits, is income generation. With interest rates becoming more normalized in recent years, bonds can represent a more significant source of incremental income. There are reasons to think that interest rates may remain at attractive levels for a while to come, especially if the economy continues to grow.

To illustrate, here is a chart of the annual income return from Vanguard’s flagship Total Bond Market ETF, representing the broad U.S. investment-grade fixed-income market. Notice that the last three years have crossed above the 3% annual income line to over 4%, up from less than 2% in 2021 [3]

The discussion above once again underlies the importance of structure when designing, implementing, and maintaining investment portfolios. A sound structure is grounded in a clear awareness of your income and liquidity needs, as well as growth priorities to provide for these needs in the future. It is constructed with an informed understanding of the realities of inflation, economic cycles, and world events, and the market volatility that often results. It is supported by confidence and discipline that take action to strengthen your ballast after prolonged periods of steady winds and promote calm, allowing the ballast to do its job when storms reappear.

(1) https://en.wikipedia.org/wiki/Vasa_(ship)

(2) Source: portfoliovisualizer.com. Hypothetical portfolios consisting of US and foreign stocks combined with short-term investment grade bonds and a 2% allocation to cash (rebalanced annually with no fees, expenses or taxes)

(3) Morningstar Direct

All information is from sources deemed reliable, but no warranty is made to its accuracy or completeness. This material is being provided for informational or educational purposes only, and does not take into account the investment objectives or financial situation of any client or prospective client. The information is not intended as investment advice, and is not a recommendation to buy, sell, or invest in any particular investment or market segment. Those seeking information regarding their particular investment needs should contact a financial professional. Coyle, our employees, or our clients, may or may not be invested in any individual securities or market segments discussed in this material. The opinions expressed were current as of the date of posting but are subject to change without notice due to market, political, or economic conditions. All investments involve risk, including loss of principal. Past performance is not a guarantee of future results.

Copyright © 2023 Coyle Financial Counsel. All rights reserved.

Start the conversation today by reaching out to our team.